Ready to learn more?

Explore More

Personal Finance

Making the Switch From Federal Employee to Corporate Worker Successfully

April 3, 2025

The buyouts and layoffs of federal employees initiated in January 2025 might lead you to move into the private sector. Going through a career transition for any reason can be scary but switching from the public sector to a corporate job comes with a particular set of considerations.

In addition to the difference in benefits, transitioning from a federal government job to a career in the private sector (generally a corporate job) can come with a variety of changes you didn’t expect. From negotiating your salary to adjusting retirement savings amounts and planning for potential bonus payouts, you’ll find that some of these differences might suit you, but they could also create new financial decisions that require careful planning.

Before you have to make these choices, though, you may be experiencing or preparing for a big drop in household income if your job gets terminated, while also brushing up on your interviewing skills and looking for the right job opportunity. Survey results show that the top barrier to a career change is lack of financial security, and the next biggest challenge is being unsure which field to enter.1 Those statistics could apply to anyone navigating a change in their career, whether chosen or not.

Below, we’ll explore choices you may face before and after transitioning to the private sector and how your decisions could impact your financial success.

First of all, if you’ve lost your job or anticipate being let go in the near future (such as due to the January 2025 buyout), take steps to help minimize the impact on your financial security. Be sure to get all the information you need from the Office of Personnel Management (OPM) or your employer to help determine your income and benefits going forward.

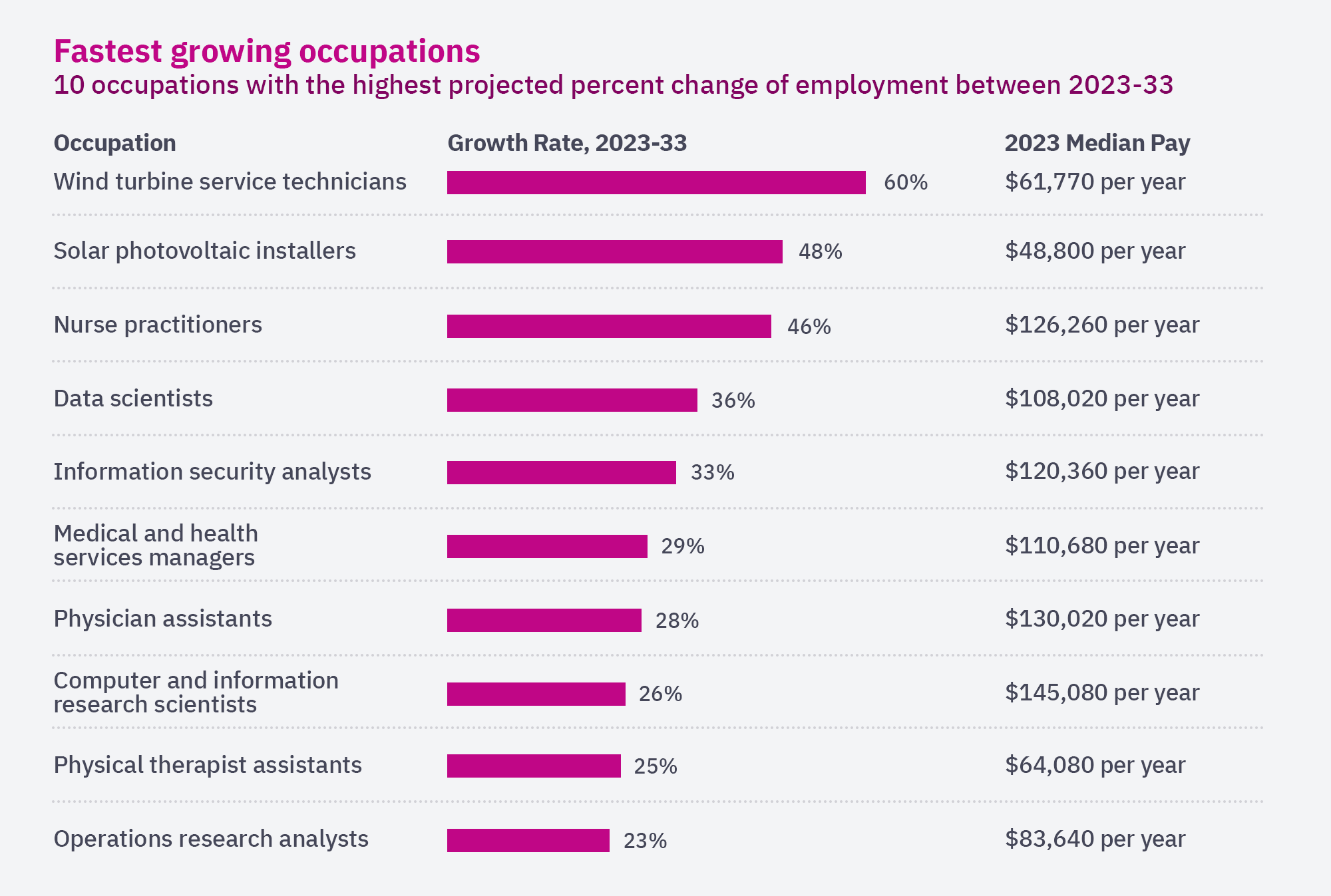

The prospect of finding a private sector job may seem daunting, but many skills gained in government roles, such as project management, regulatory knowledge, and leadership, are highly valued in the private sector. Take some time to educate yourself on fields that interest you. Identify how your government experience, particularly universal skills and achievements, can transfer to private sector roles and communicate them effectively in an interview. You are likely to be asked to give examples of situations you successfully handled in your job. Focus your resume on outcomes and impacts you’ve made, and keep it concise—no more than two pages. Research companies and their culture to find the right fit — remember, you are also interviewing potential employers. Maintain a networking mindset and actively engage in industry events, social media, and associations.

Private sector compensation packages can vary widely. Consider salary, potential bonuses, equity options, health benefits, and retirement plans when evaluating job offers. Don’t be afraid to negotiate your salary. You may also be able to negotiate on benefits depending on your job level. Research the industry standards for a position to ensure you’re getting a fair offer. While salary is certainly important, this may be a good opportunity to honor your work-life balance needs with a job that’s a better fit.

Typically, once you receive a job offer in the private sector, you’ll quickly be asked to make financial decisions related to benefits. You may also experience changes in cash flow, depending on your new salary and other compensation. It is important to understand how your choices will affect your short- and long-term financial goals.

As you close out one chapter in your career and begin a new one, it may be the right time to create or modify your financial plan. When transitioning careers, it’s important to have clear, long-term goals as your focus. Those can change over time, as will the path along the way, but having a target can help you make important financial decisions. Switching from federal government employment to private sector employment brings new and different options that should be navigated carefully to help ensure financial success.

Mercer Advisors has extensive experience in assisting clients who are going through major job or career transitions, including federal employees. Our seasoned team can collaborate with you to develop a financial plan that aligns with your professional objectives, so you can feel confident when taking the next step.

Are you ready to simplify and amplify your (financial) life? We can help by connecting the dots of your financial life by unifying financial planning, investment management, tax, estate, insurance, and more. We’d be honored to be part of your journey. Let’s talk.

1 “21 Crucial Career Change Statistics [2023]: How Often Do People Change Jobs?” Zippia, Feb. 9, 2023.

Mercer Advisors Inc. is a parent company of Mercer Global Advisors Inc. and is not involved with investment services. Mercer Global Advisors Inc. (“Mercer Advisors”) is registered as an investment advisor with the SEC. The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. For financial planning advice specific to your circumstances, talk to a qualified professional at Mercer Advisors.

Tax preparation and tax filing are a separate fee from our investment management and planning services. Mercer Advisors is not a law firm and does not provide legal advice to clients. All estate planning document preparation and other legal advice is provided through select third parties unaffiliated to Mercer Advisors. Mercer Global Advisors has a related insurance agency. Mercer Advisors Insurance Services, LLC (MAIS) is a wholly owned subsidiary of Mercer Advisors Inc. MAIS provides individual life, disability, long term care coverage, and property and casualty coverage through various insurance companies. For Mercer Global Advisors clients who wish to purchase insurance products, MAIS has entered into a non-exclusive referral agreement with Strategic Partner(s), where the Strategic Partner will provide necessary services relative to the marketing, placement, and servicing of the insurance products, including without limitation preparing and presenting illustrations, supporting the underwriting process, assisting with the completion and execution of applications, delivering policies, and servicing in-force business. MAIS and the Strategic Partner will be listed as either “agents” or “co-agents” on the policies. While Mercer Global Advisors does not receive a referral fee, Strategic Partner receives a percentage of the commission revenue. MAIS and Strategic Partner do have a revenue sharing agreement.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark, the CERTIFIED FINANCIAL PLANNER™ certification mark, and the CFP® certification mark (with plaque design) logo in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

CHARTERED RETIREMENT PLANNING COUNSELOR℠ and CRPC® are trademarks or registered service marks of the College for Financial Planning in the United States and/or other countries.

April 3, 2025