For much of 2023 and 2024, the market was dominated by seven high-flying tech stocks – Amazon, Apple, Google, Meta (Facebook), Microsoft, Nvidia, and Tesla – that were dubbed the Magnificent Seven. But beginning with the great rotation last summer, and the recent tumbling of these stocks, it seems their reign may be coming to an end.

Points to consider

- Successful stocks have a history of struggling to stay on top. The companies at the top of the market, by definition, have enjoyed an incredible run. There’s always a temptation to look wistfully at those companies – wishing you’d bought them a long time ago – and wonder if you ought to weight your portfolio more heavily toward the winners. History suggests high-flyers don’t always have an easy path forward.

- Broad diversification strategy can help protect your portfolio against downturns. History and academic research show that broad diversification, as we recommend for our portfolios, is the strategy that can better protects us from downturns. Over time, broad diversification typically leads to higher expected returns with lower expected volatility. We’re seeing that play out right now.

- If a portfolio is overweight Magnificent Seven tech stocks, it’s not too late to diversify that concentrated position. In hindsight, it’s easy to find a stock’s peak and wish you’d picked that day to sell all your holdings. In reality, however, someone who has built a large position in Magnificent Seven companies has likely done quite well over the last few years despite those stocks stumbling this year. Those investors may still have a very large capital gain in their position and would likely still benefit from a diversification strategy.

The context

For two years the Magnificent Seven dramatically outpaced the rest of the stock market. From the start of 2023 until the Magnificent Seven collectively reached their peak on Dec. 17, 2024, the stocks climbed 267%, compared to a (still very strong) 57.6% climb for the overall S&P 500, according to Bloomberg data.

Since reaching their respective record high closes, the Magnificent Seven stocks are down as of Friday, March 28, 2025, between 14% – for Apple, which has dropped the least – to Tesla, which is down 43% from its peak close.

Stretched valuations

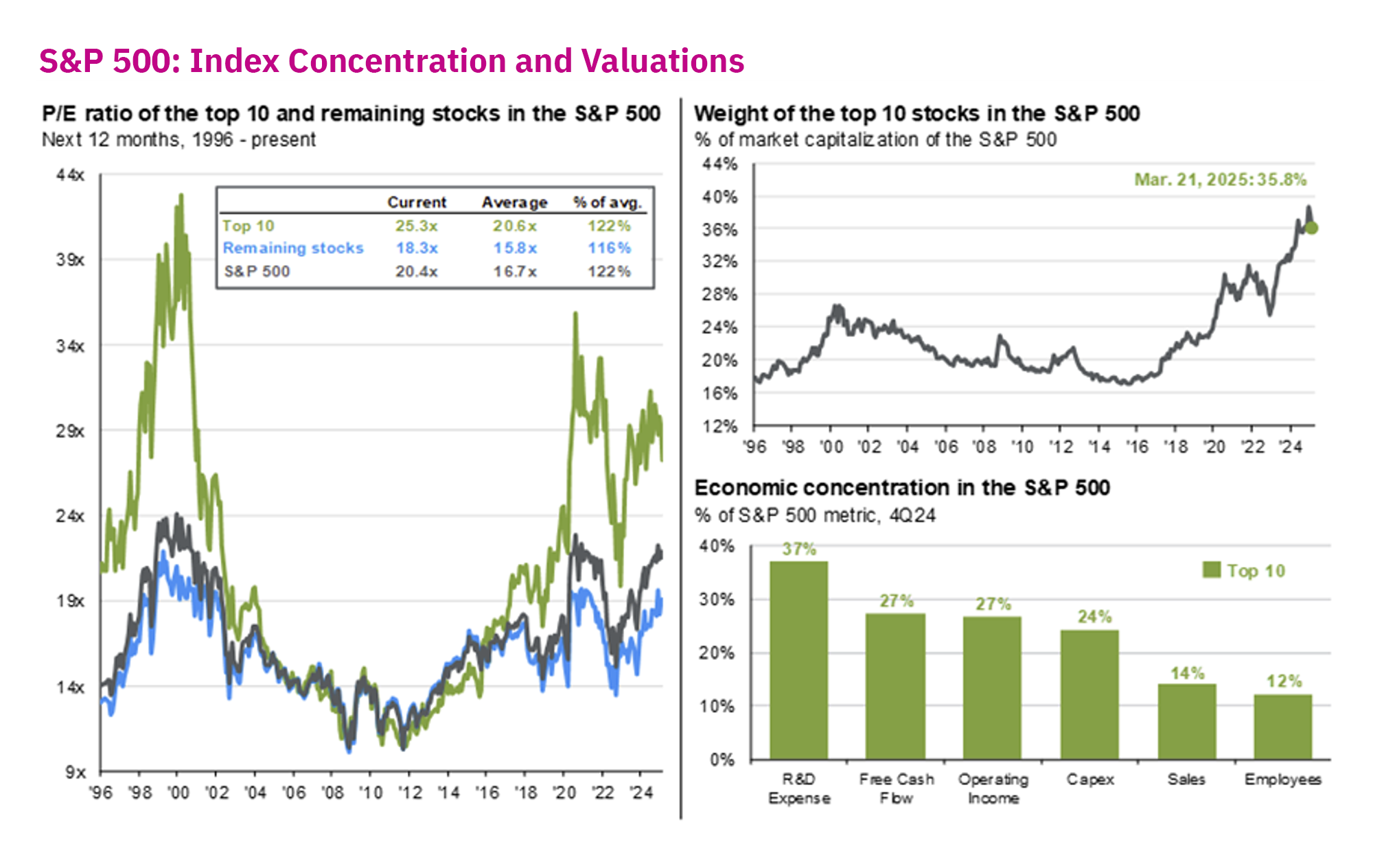

While we often say there are no laws of physics in the financial markets, it is true that the valuations of the leading tech companies have been stretched.

Consider the left panel in the chart below. Even after their recent stumbles, the top 10 stocks in the S&P 500 have been trading at around 20.6 times earnings, compared to 15.8 times of the rest of the market.

But as the chart shows, it’s not always the case that the leading stocks have valuations that exceed their earnings, compared to the rest of the market. On the contrary, from 2002 to 2018 – nearly the entirety of the last two bull markets – the price/earnings ratio of the top 10 stocks wasn’t that different than the other 490 stocks in the S&P 500 and, in fact, the top 10 stocks sometimes had lower P/E ratios.

The struggle to stay on top

The pattern playing out now is one we’ve seen repeatedly throughout history. The top 10 stocks, which often seem invincible, sometimes struggle to remain on top.

In 2015, only four of the top 10 companies (those in blue) remain on the list today. From 2010, only Microsoft and Apple remain. None of the top 10 companies from 1985 to 1995 were still on the list by 2020.

Consider some of the companies that once sat on the list, like General Electric (GE). It was once considered the best managed company in America and Fortune magazine dubbed GE CEO Jack Welch the “manager of the century.” It went from the top company in 2005, to hitting trouble in the financial crisis, to being removed from the Dow Jones Index by 2018.

IBM was synonymous with personal computers. It was of course true that computers were the future, but this doesn’t mean the early winner of a new technology will be the winner down the road – even if the technology itself truly is revolutionary.

The benefits of diversification

We may not know when or how strongly the tide will turn, and indeed it’s quite likely that some of today’s top stocks will remain near the top. We, of course, still generally recommend owning these stocks as part of diversified portfolios. The point isn’t to avoid them entirely.

But we prepare for the inevitability that some winners will turn into losers, by pursuing broad diversification. In recent years, we’ve often heard people express concern about bonds or international stocks. “Why own these assets when they’ve had a period underperforming?”

The answer is that we include those assets for moments like today.

- Year-to-date, we’ve seen the Magnificent Seven fall by 12%

- The other 493 stocks in the S&P 500 have been up about 0.4%

- International developed market stocks (excluding the U.S.) are up about 9% year-to-date

- Emerging market stocks are up over 5%

- The Bloomberg U.S. Aggregate Bond Market Index is up 2.6%

If you’re not diversified, it’s not too late to begin

As we said at the outset – it can be agonizing to look at a recent stock peak and think about what one missed. But for investors who have been overweight one of the Magnificent Seven stocks (or overweight any stock for that matter), it’s certainly not too late to develop a strategy to diversify out of that position.

One of the big mistakes that investors make with concentrated positions, of course, is not planning for the tax consequences of diversifying. An investor who acquired their Magnificent Seven stocks over a long period of time would likely still be sitting on a large unrealized capital gain. If they sold their position without a strategy, they could face a significant tax bill. Thus, developing a systematic strategy to unwind concentrated positions over time remains the key to successful diversification.

Click here for past insights about the recent market volatility and other interesting topics. Not a Mercer Advisors client but interested in more information? Let’s talk.

Mercer Advisors Inc. is a parent company of Mercer Global Advisors Inc. and is not involved with investment services. Mercer Global Advisors Inc. (“Mercer Advisors”) is registered as an investment advisor with the SEC. The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. For financial planning advice specific to your circumstances, talk to a qualified professional at Mercer Advisors.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy or product made reference to directly or indirectly, will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio. Diversification does not ensure a profit or guarantee against loss. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark.

This document may contain forward-looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Home » Insights » Market Commentary » A Reversal for the Magnificent Seven

A Reversal for the Magnificent Seven

David Krakauer, CFA®, CRPS®

Sr. Director, Portfolio Management

Lessons from the abrupt tumble in the Magnificent Seven tech stocks which had led the markets in 2023 and 2024.

For much of 2023 and 2024, the market was dominated by seven high-flying tech stocks – Amazon, Apple, Google, Meta (Facebook), Microsoft, Nvidia, and Tesla – that were dubbed the Magnificent Seven. But beginning with the great rotation last summer, and the recent tumbling of these stocks, it seems their reign may be coming to an end.

Points to consider

The context

For two years the Magnificent Seven dramatically outpaced the rest of the stock market. From the start of 2023 until the Magnificent Seven collectively reached their peak on Dec. 17, 2024, the stocks climbed 267%, compared to a (still very strong) 57.6% climb for the overall S&P 500, according to Bloomberg data.

Since reaching their respective record high closes, the Magnificent Seven stocks are down as of Friday, March 28, 2025, between 14% – for Apple, which has dropped the least – to Tesla, which is down 43% from its peak close.

Stretched valuations

While we often say there are no laws of physics in the financial markets, it is true that the valuations of the leading tech companies have been stretched.

Consider the left panel in the chart below. Even after their recent stumbles, the top 10 stocks in the S&P 500 have been trading at around 20.6 times earnings, compared to 15.8 times of the rest of the market.

But as the chart shows, it’s not always the case that the leading stocks have valuations that exceed their earnings, compared to the rest of the market. On the contrary, from 2002 to 2018 – nearly the entirety of the last two bull markets – the price/earnings ratio of the top 10 stocks wasn’t that different than the other 490 stocks in the S&P 500 and, in fact, the top 10 stocks sometimes had lower P/E ratios.

The struggle to stay on top

The pattern playing out now is one we’ve seen repeatedly throughout history. The top 10 stocks, which often seem invincible, sometimes struggle to remain on top.

In 2015, only four of the top 10 companies (those in blue) remain on the list today. From 2010, only Microsoft and Apple remain. None of the top 10 companies from 1985 to 1995 were still on the list by 2020.

Consider some of the companies that once sat on the list, like General Electric (GE). It was once considered the best managed company in America and Fortune magazine dubbed GE CEO Jack Welch the “manager of the century.” It went from the top company in 2005, to hitting trouble in the financial crisis, to being removed from the Dow Jones Index by 2018.

IBM was synonymous with personal computers. It was of course true that computers were the future, but this doesn’t mean the early winner of a new technology will be the winner down the road – even if the technology itself truly is revolutionary.

The benefits of diversification

We may not know when or how strongly the tide will turn, and indeed it’s quite likely that some of today’s top stocks will remain near the top. We, of course, still generally recommend owning these stocks as part of diversified portfolios. The point isn’t to avoid them entirely.

But we prepare for the inevitability that some winners will turn into losers, by pursuing broad diversification. In recent years, we’ve often heard people express concern about bonds or international stocks. “Why own these assets when they’ve had a period underperforming?”

The answer is that we include those assets for moments like today.

If you’re not diversified, it’s not too late to begin

As we said at the outset – it can be agonizing to look at a recent stock peak and think about what one missed. But for investors who have been overweight one of the Magnificent Seven stocks (or overweight any stock for that matter), it’s certainly not too late to develop a strategy to diversify out of that position.

One of the big mistakes that investors make with concentrated positions, of course, is not planning for the tax consequences of diversifying. An investor who acquired their Magnificent Seven stocks over a long period of time would likely still be sitting on a large unrealized capital gain. If they sold their position without a strategy, they could face a significant tax bill. Thus, developing a systematic strategy to unwind concentrated positions over time remains the key to successful diversification.

Click here for past insights about the recent market volatility and other interesting topics. Not a Mercer Advisors client but interested in more information? Let’s talk.

Mercer Advisors Inc. is a parent company of Mercer Global Advisors Inc. and is not involved with investment services. Mercer Global Advisors Inc. (“Mercer Advisors”) is registered as an investment advisor with the SEC. The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. For financial planning advice specific to your circumstances, talk to a qualified professional at Mercer Advisors.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy or product made reference to directly or indirectly, will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio. Diversification does not ensure a profit or guarantee against loss. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark.

This document may contain forward-looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Explore More

Q2 Market Outlook: What Does Q2 Hold for Investors?

After the Fall: Four Questions for Investors: Insights From Our CIO

The Fallacy of Selling and Waiting Until Markets Calm Down: Insights From Our CIO