Did you know that Social Security income is taxable, and that you may have to repay benefits if your income is higher than a certain threshold? Is it surprising that the Social Security Administration deems 67 to be the full retirement age? While these facts may be new to you, specific strategies can potentially mitigate your tax burden and help maximize your benefits. We’ve created a brief guide for deriving the most income potential from your Social Security benefits. Keeping in mind four key concepts is critical: be aware of income limits, determine how your benefits are taxed, consider the impact of a Roth IRA conversion, and determine the optimal age to begin collecting benefits.

1. Be aware of income limits

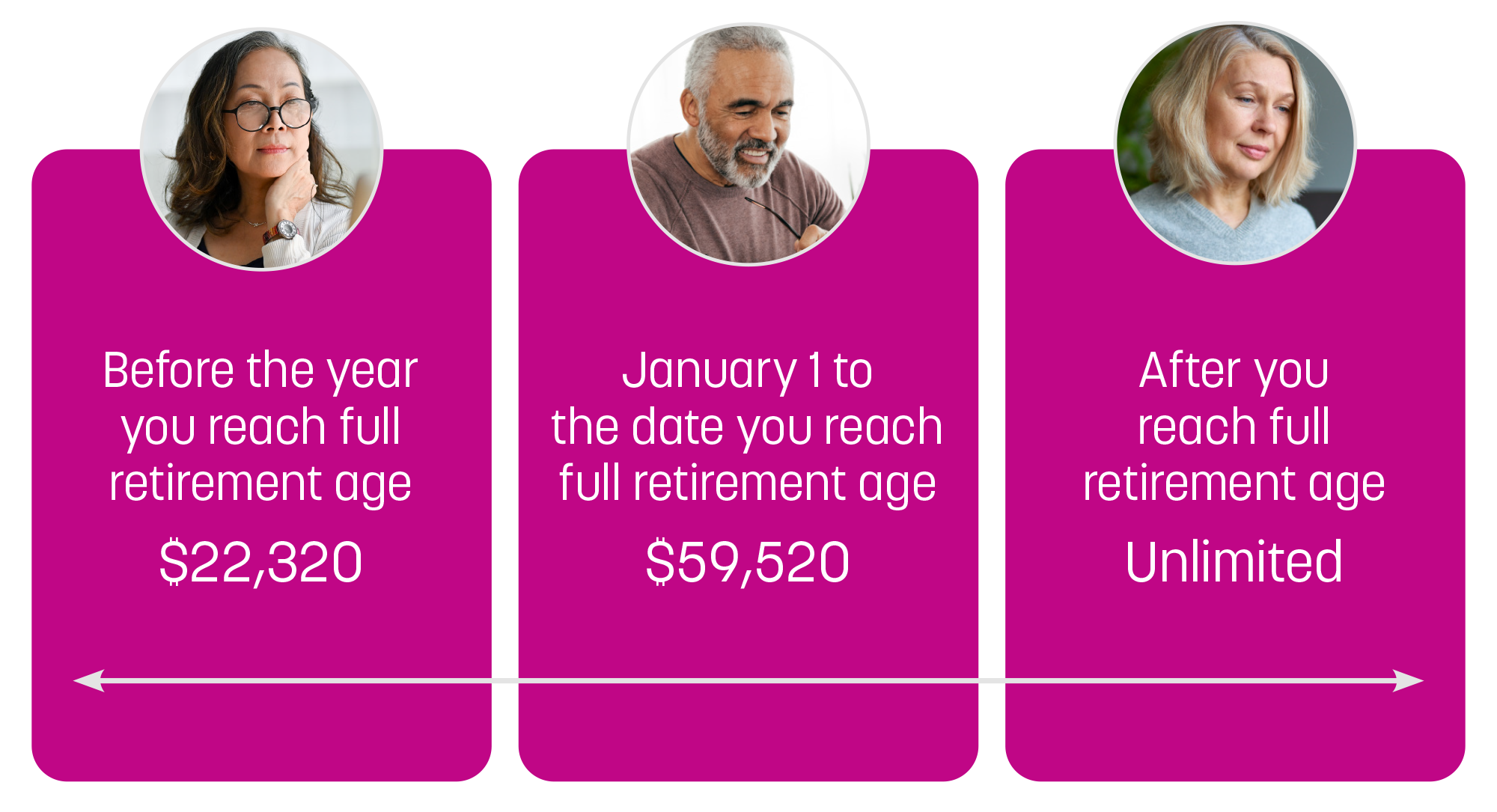

If you collect Social Security before the full retirement age of 67, there are limits to how much income you can earn from work before you must repay some benefits. “Work” is defined as W-2 income (salary, hourly, bonuses, and commissions) as well as net income from self-employment (business income). It doesn’t include income from interest or dividends. In the year when you reach full retirement age, you’re allowed a higher income threshold than in the preceding year.

Jenna, a teacher, began collecting Social Security at age 62, fearing an early death due to bad genetics. In 2024, at age 63, she’ll work as a school aide and earn $30,000. Because Jenna has not yet reached full retirement age, she’s subject to an income limit. In 2024, the limit is $22,320. Jenna will earn $7,680 more than that threshold ($30,000 minus $22,320). Social Security will deduct $1 of benefits for every $2 over the threshold—in Jenna’s case, this will be $3,840 of the benefits paid to her.

Cameron, an engineer, began collecting Social Security in 2023 at age 66. In 2024, his income will be $200,000 (or $16,667 per month). Because Cameron will reach full retirement age on August 1, there will be a reduction in benefits from January through July (when his earnings will be $116,669). His income will be above the annual limit by $57,149 ($116,669 minus $59,520). Social Security will deduct $1 of benefits for every $3 over the threshold—in Cameron’s case, this will be $19,050 in benefits during the first seven months of 2024. From August 1 to December 31, Cameron will not be subject to an income threshold.

Felicia is 68 and began collecting Social Security in 2023 at age 67. In 2024, she’ll make $1,000,000 as an actress. Because she has already reached full retirement age, there will be no income limit and therefore no reduction in her Social Security benefits.

2.Determine how your Social Security benefits are taxed

A common misconception is that Social Security benefits are tax-free, but this is not necessarily the case. Here are some guidelines to help determine how much of your Social Security benefits will be taxed. Depending on income and filing status, up to 85% of benefits may be taxable. On the brighter side, the remaining 15% will always be tax-free.

Table 2: Social Security Taxation, by Income and Filing Status

Adjusted gross income (AGI) (line 11 of Form 1040 for tax-year 2023 minus Social Security on line 6b)

+ Tax-exempt interest (line 2a of Form 1040 for tax-year 2023)

+ Half of Social Security benefits (SSA-1099, box 5)

= Combined income

3.Consider the impact of a Roth IRA conversion

Roth IRA conversion is a strategy for moving money from a taxable IRA to a tax-free IRA. Typically, this process is reported in the tax return for the year when the conversion occurred. There are many reasons to consider a Roth IRA conversion:

This is currently one of the lowest taxation environments, with rate increases scheduled for 2026 when the Tax Cuts and Jobs Act of 2017 expires.

Principal, earnings, and assets of a Roth IRA can grow tax-free and be withdrawn tax-free.

Roth IRA has no required minimum distributions (RMDs) during the owner’s lifetime (and, potentially, the lifetime of their spouse). Conversely, a traditional IRA requires distributions by individuals:

If born in 1959 or earlier, 73 is the age when you must begin taking RMDs

If born in 1960 or later, 75 is the age when you must begin taking RMDs

With recent passage of the SECURE 2.0 Act, changes have been made in the inheritance of an IRA by a non-spouse. Now, when an adult child inherits an IRA from their parent, they’re typically required to take out all of the money within a 10-year period. This could lead to a much higher tax burden than previous rules.

There may be some drawbacks, however, to a Roth IRA conversion:

You’ll pay taxes now when you could potentially pay them later.

If an inheritance is being considered and the beneficiary has a lower income, they could pay less tax than you would during a conversion.

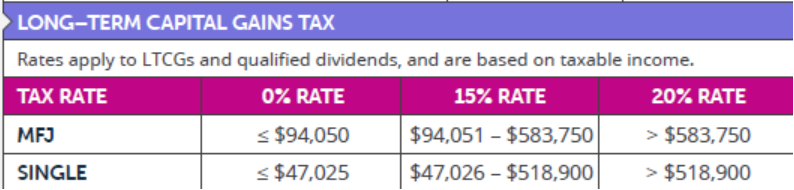

Capital gains income (e.g., stock sales) could move you from a 0% rate to 15%.

Table 3: Long-term Capital Gains Tax Brackets

Source: Internal Revenue Service

Beware the “tax torpedo.” This concept is threatening not only in name but also in execution: higher income means greater taxation of Social Security benefits (see Table 3 above). For every dollar of income above the threshold of $34,000 for a single filer and $44,000 for married filing jointly, an additional $0.85 of Social Security benefits will be taxed—until a maximum of 85% of benefits is reached. For example, if you earn $1 more in interest, that dollar will be taxed as income and another $0.85 of Social Security benefits will be taxed. Thus, $1 of interest income actually means $1.85 of taxable income, so the marginal tax rate is 185% of the tax bracket.1 This is why the term “tax torpedo” was coined—an increase in income can nearly double the amount of tax due, because Social Security benefits must be included.

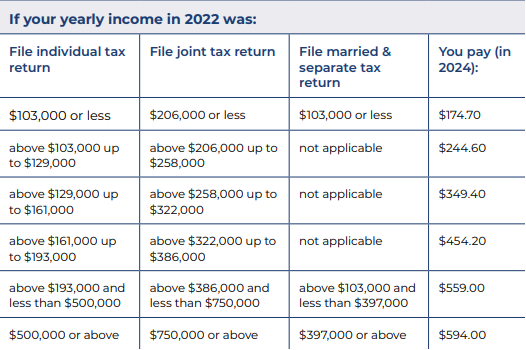

A Roth IRA conversion can increase the amount of AGI in a tax return. Not only will more Social Security income be taxable, but Medicare premiums can also be affected. The income-related monthly adjustment amount (IRMAA) determines the Medicare premium that must be paid. Social Security uses the income tax return from two years prior, so a Medicare premium for 2024 will be based on the reported income in a 2022 tax return. In Table 4, you can see that when modified AGI moves you into a higher bracket, Medicare premiums for that year may also increase.

Table 4: Medicare Premiums, by Income and Filing Status

4.Determine the optimal age to begin collecting benefits

If only we had a crystal ball that could foresee our age at death, then we’d know exactly when to begin collecting Social Security benefits. Unfortunately (or fortunately, depending on your viewpoint), we must instead use other tools in making this decision. Three different benefits are available to individuals, assuming eligibility has been met:

Retirement — when you work and collect benefits based on your earnings record

Spousal — when one spouse hasn’t worked or earned as much as the other spouse, the non-worker can collect half of their spouse’s benefits

Survivor — when one spouse passes away, the lesser of their individual benefits disappears while the greater remains for the survivor; it may make sense for the high-earner to delay collecting Social Security so that they receive the most-possible benefits while alive (and so their spouse continues to receive them afterward)

When determining the best strategy, you must consider which benefits are applicable and what they would amount to. If no one in your family has lived past age 65, you might decide to collect benefits sooner rather than later. If longevity is on your side, delaying Social Security could be a better option. You should also evaluate the health of the Social Security system itself. In their 2023 annual report, trustees of the Social Security fund said it will be capable of paying 100% of benefits until 2033, at which point the rate will fall to 77%. While this is a staggering decline, Congress has many tools that can help address the deficit in advance, such as increasing the full retirement age, raising the Social Security tax rate above 6.2%, raising the amount of wages subject to Social Security tax above $168,000, or reducing benefits.

If no other assets or income are available to you, then collecting Social Security may be your only option. Benefits increase by 8% for every year you defer after reaching full retirement age. Conversely, benefits decrease by as much as 30% if you collect them early. Waiting until full retirement age—or later, if possible—is the best strategy for a higher payout.

Table 5: Social Security Payout, by Age, for Individuals Born in 1960 and Later

Social Security benefits calculations may seem like rocket science, but we’ve highlighted a few savvy strategies to help you maximize benefits while minimizing the tax burden. If you’re still uncertain or need help in determining which Social Security tax strategies are best suited to your portfolio, contact your wealth advisor today. If you’re currently looking for an advisor, let’s talk.

1Morningstar, “How Retirees Can Avoid the ‘Tax Torpedo,’ March 8, 2023.

Mercer Advisors Inc. is a parent company of Mercer Global Advisors Inc. and is not involved with investment services. Mercer Global Advisors Inc. (“Mercer Advisors”) is registered as an investment advisor with the SEC. The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. The hypothetical examples are for illustrative purposes. For financial planning advice specific to your circumstances, talk to a qualified professional at Mercer Advisors.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark, the CERTIFIED FINANCIAL PLANNER® certification mark, and the CFP® certification mark (with plaque design) logo in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements. The CDFA® and Certified Divorce Financial Analyst marks are the property of the Institute for Divorce Financial Analysts, which reserve sole rights to their use, and are used by permission.